You want to bet interest rates are coming down in the next 2 years?

I don’t.

Because it’s my view that interest rates are now returning to normal levels. Remember the 1970s? 80s? 90s? Or even the early 2000s?

When I was a teenager in the mid ’90s, I remember my parents complaining about their mortgage payments but not their mortgage rate, which was around 7%, normal at the time.

Going back further, interest rates in the 1970s bounced around the double digits. 1980s rates often ranged between 8 to 10% range. Even the early 2000s saw rates between 5 and 6%.

If you ask me, today’s buyers have a serious case of recency bias when it comes to interest rates. They think rates will come down because that’s what they’ve been used to for the last 10 years.

Recency bias is a psychological tendency we all fall victim to. We make decisions about the future based on the most recent information and events, because that’s what’s fresh in our minds.

And when it comes to mortgage rates, so many buyers wistfully dream of a return to 2 to 3% interest rates of the 20-teens. (I had one client score a 1.69% interest rate in June 2020 during the pandemic.)

But it would be a mistake to wait or hope for rates to come down. It would be worse to base your decision to buy on rates coming down.

The golden era of low interest rates is over. I’ll prove it to you.

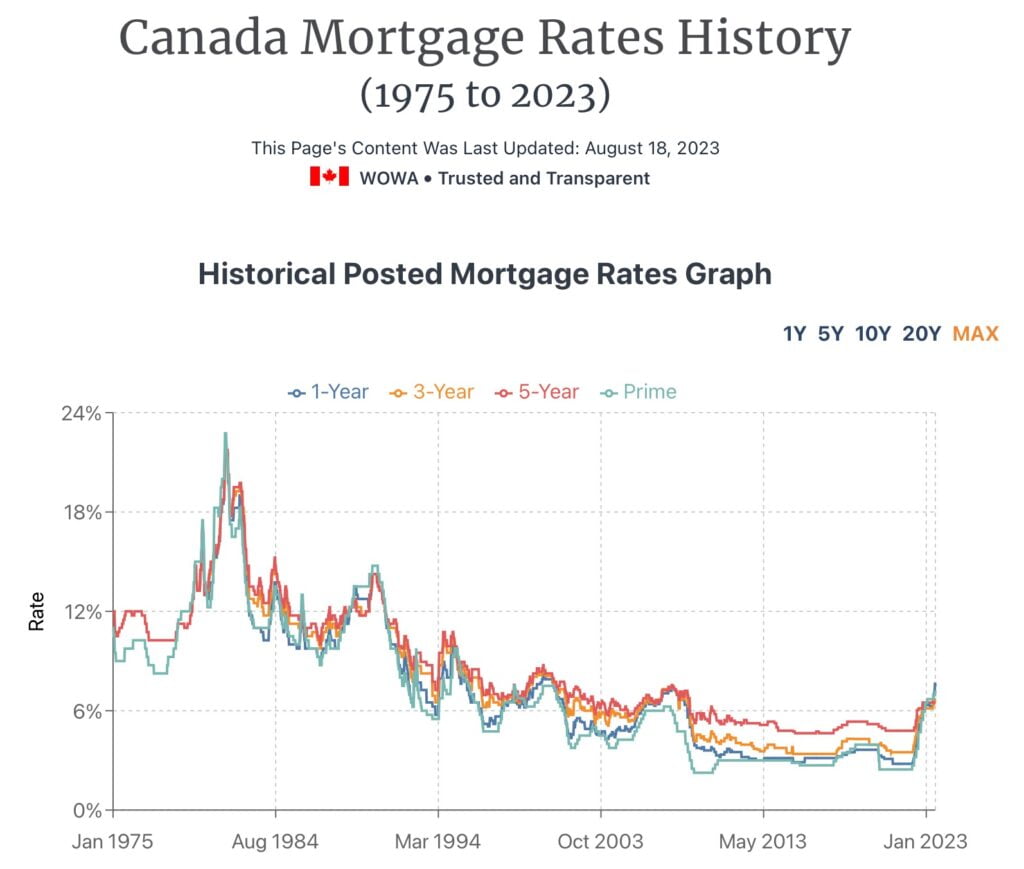

Look at historical rates dating back half a century to draw comparisons with today:

Source: https://www.toonpool.com/cartoons/Interest%20rate%20raise_120111

One look at this graph shows rates are just now returning to pre-2010 levels. The collapse of financial markets in the fall of 2008 ushered in a period of unprecedented low interest rates.

You can run your finger all the way to the left–1975–and you’ll see nothing but rising rates.

Some buyers visiting my open houses tell me that they’re in a holding pattern, hoping that rates will come down. This reminds me of the filmmaker James Cameron’s line: “Hope is not a strategy.”

Reading between the lines, what some people are saying is that they can’t afford today’s payments. Understood.

But for buyers waiting to pull the trigger on a home purchase in the hopes rates come down, I got news for you: Interest rates aren’t coming down anytime soon, and there’s a simple reason why.

The Bank of Canada has a mandate to wrestle inflation down to 2% levels. But the latest CPI numbers are expected to come in at close to 4%, which is still way too high, for the BOC to consider lowering rates. Inflation may be far more entrenched than we thought 16 months ago.

It could take years before inflation returns to a steady 2%.

Get used to it, friends. Today’s rates are the new normal.